Much work has been done in 2016 to increase protection for consumers utilizing payday loan services across the country. Credit Counselling Canada members nationwide have participated in government consultations to ensure consumers can access short-term credit during financial emergencies without undue hardship.

Credit Counselling Canada is pleased with many of the outcomes of these consultations, including the Ontario government proposing to lower fees on payday loans to $15 on $100 by 2018. A lower rate will ease the financial burden on consumers when they are at a difficult time in their lives.

Our position is that while such amendments are a start, they are not a sufficient solution to the payday loan problem.

While the cost of borrowing is certainly problematic, we believe that payday borrowing is a symptom of much deeper financial problems. These include a lack of financial literacy and consumer protection. To protect vulnerable consumers, there should be additional payday loan regulations put in place, not only in Ontario but across all jurisdictions.

1. Increase transparency around rates.

Consumers using payday loans may be vulnerable in the sense that the average consumer does not understand the actual calculation of interest for payday loans.

We prefer lowering the fee but more importantly, we recommend a requirement for the rate to be expressed as an annualized rate. Consumers see $21/$100 and think this is 21% which compares reasonably with other credit products and interest rates. Consumers do not realize that the annualized rate is more like 479%. Having the rate expressed in an annualized rate makes the comparison with other credit products clearer and creates a better understanding of the cost up front.

2. Decrease repeat borrowing. Ie. the payday loan cycle.

We are concerned about the prevalence of repeat borrowing. Many consumers are unaware of the longer-term consequences of taking the maximum possible amount when applying for their first payday loan. For example, they will only have $X of their pay remaining after they pay for their first loan and the cycle begins.

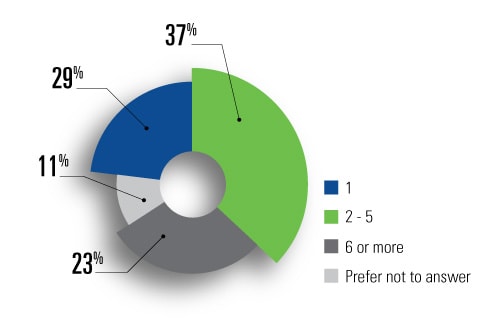

How many times do you estimate you have used a payday loan in the last three years? (FCAC national survey of 1,500 Canadian payday loan users)

British Columbia has dealt with this by implementing a regulation that says if you take out three payday loans within a 62-day period, a repayment option will be triggered, which allows the borrower to repay the outstanding indebtedness over two or three pay periods. This gives the borrower a fair chance to get back on track and end the cycle.

To give borrowers a chance to repay their loans in full as opposed to paying debt with debt, as proposed in New Brunswick, consumers should be limited in the maximum amounts to be borrowed based on net income. New Brunswick has proposed the total amount that can be borrowed by any one person be at 30% of net income as compared to 50% which exists in other jurisdictions.

In addition to changing borrowing periods and maximum borrowing limits, repeat borrowing may be decreased by increasing reporting of payday loans to credit bureaus. This practice could help regulate multiple concurrent loans and give consumers the opportunity to increase their credit ratings when they properly pay back money borrowed.

With current legislation, repeat borrowing often creates a dependency on payday loans which in our experience only ends in personal bankruptcy. This occurs after months of financial stress trying to repay with an even larger psychological effect on the borrower and their families.

3. Incentives for proper payday loan repayment.

Options on lending products where paying on time reduces the interest or even opportunities for lowering interest when the total amount of credit is reduced are incentives for good repayment.

Such incentives could include: At the request of a borrower who has successfully repaid three prior payday loans from a lender over the preceding 12-month period, the lender be required to either grant a payday loan extension at a rate of 5% or convert the payday loan to an installment loan. The installment loan would be repaid over the next four pay periods. The applicable rate for the installment loan may be 7% of the principal outstanding amount of the principal owing when the installment loan was requested.

As previously mentioned, reporting of payday loans to credit bureaus would also provide consumers with an incentive to build their credit ratings. This could potentially increase their prospects of qualifying for more traditional loans.

4. Development of new options.

People using a payday loan are frequently facing circumstances with significant pressure. They are already cash strapped and spend their paydays going from lender to lender to renew loans creating added expense on an already tight budget. If they are not physically going to a payday loan company, they are renewing or obtaining loans online. More online businesses are providing loans and credit than ever before. Consumers are not always aware of the jurisdiction they are dealing with. This makes it difficult to understand the associated laws and risks.

We need to be much more open to other types of credit products to assist people with short-term borrowing needs. For this reason, we support governments in making it easier for other financial institutions to develop easy to access, low-cost products to compete with payday loans. Additionally, lending circles have become popular in community development groups. These circles establish savings and borrowing concepts.

Other solutions beyond regulatory considerations should include a view to treating the underlying cause versus the symptom. Financial literacy education which addresses the root cause for high-cost borrowing is essential. In a national survey of 1,500 Canadian payday loan users conducted by the Financial Consumer Agency of Canada, self-reported financial literacy correlated with both successful budgeting and less frequent payday loan use. Helping people to understand how to plan for emergencies and how to manage when income and expenses are not aligned is critical. Choosing the right credit product is also an important feature of using credit wisely.

Together, we need to do more to meet the needs of underbanked, marginalized and vulnerable populations.